Featured

Green Building · Engineering Analysis

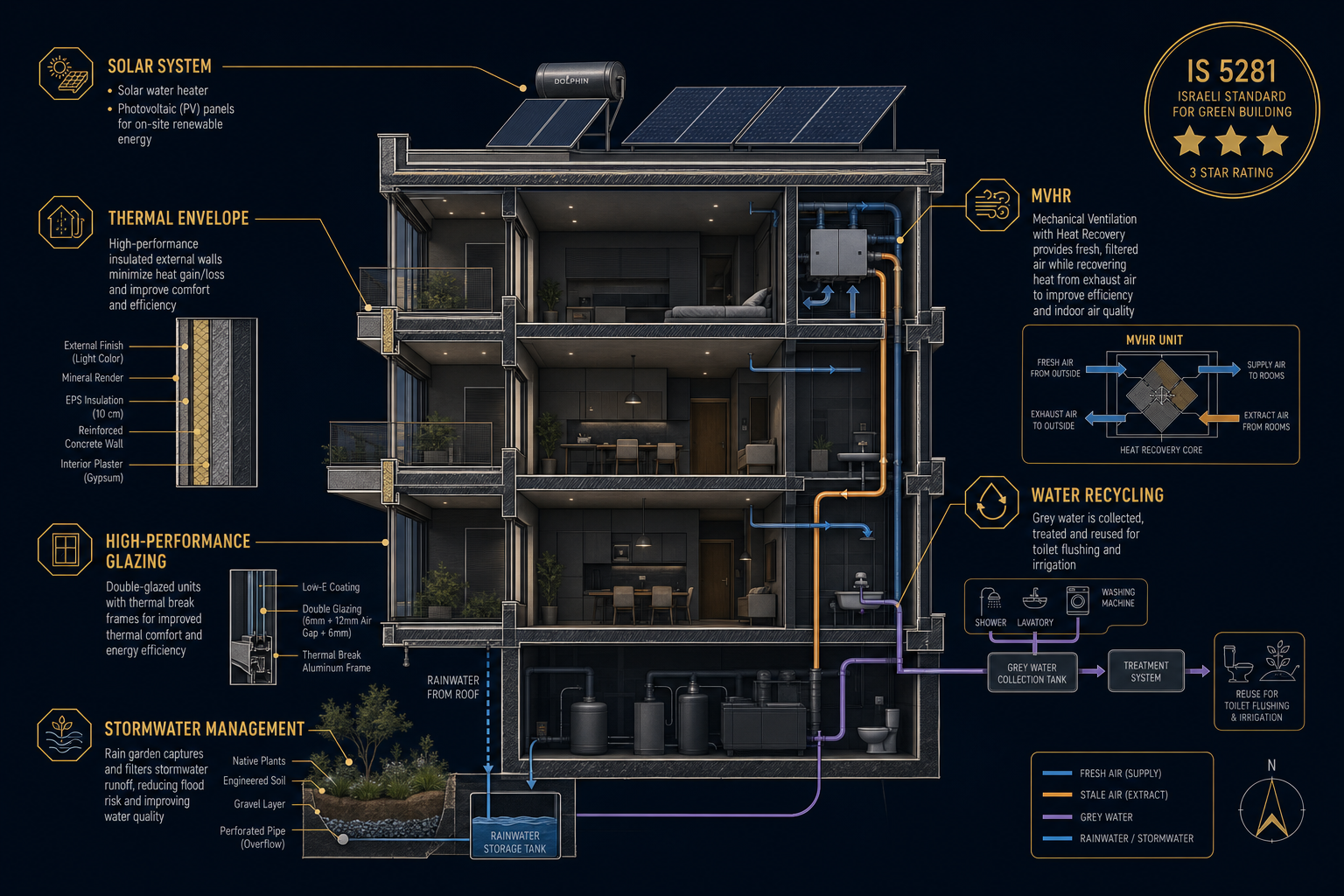

What Environmental Quality Standards Actually Cost Israeli Developers — And What They Return

IS 5281 certification from design stage vs. retrofit: the real numbers. Razore Engineering's analysis of 60+ certified projects — cost premiums, 25-year energy savings, and the three mistakes that cost developers millions.

Engineering Partner · Radiation

Dr. Liran Raz Steinkritser — Israel's Leading Radiation Engineer, and the Millions He Saves Developers Every Year

25 years. Dual MoEP licences. PhD. How Razore Engineering's senior radiation specialist turns Israel's strictest environmental thresholds into developer wins — ₪4.7M saved across three documented cases.